Revenue management is now an inputs problem.

The trade-press version of the airline-and-hotel revenue-management story between 2022 and 2025 is a model-architecture story. New AI techniques arrive; old optimization stacks retire; pricing gets smarter. That story is partially right and meaningfully misleading. The model-class running production pricing decisions in 2025 sits within the same family of demand-forecasting plus constrained-optimization architectures that ran production pricing decisions in 2018. The difference is not architectural. The difference is the inputs the model ingests and the segments the model prices against.

This is an explainer. The intent is to walk the four input-layer changes that the trade press has been generally not surfacing, with the data shape the operator class actually sees in their pricing systems. Section one looks at the data that moved into the input layer between 2022 and 2025. Section two walks the segmentation refinements that drop out of the new inputs. Section three is the operator-class question of which inputs to license, build, or capture. Section four closes with what a pricing strategy looks like when the operator question is which inputs to feed the model rather than which model to use.

Section one: the input layer that actually moved

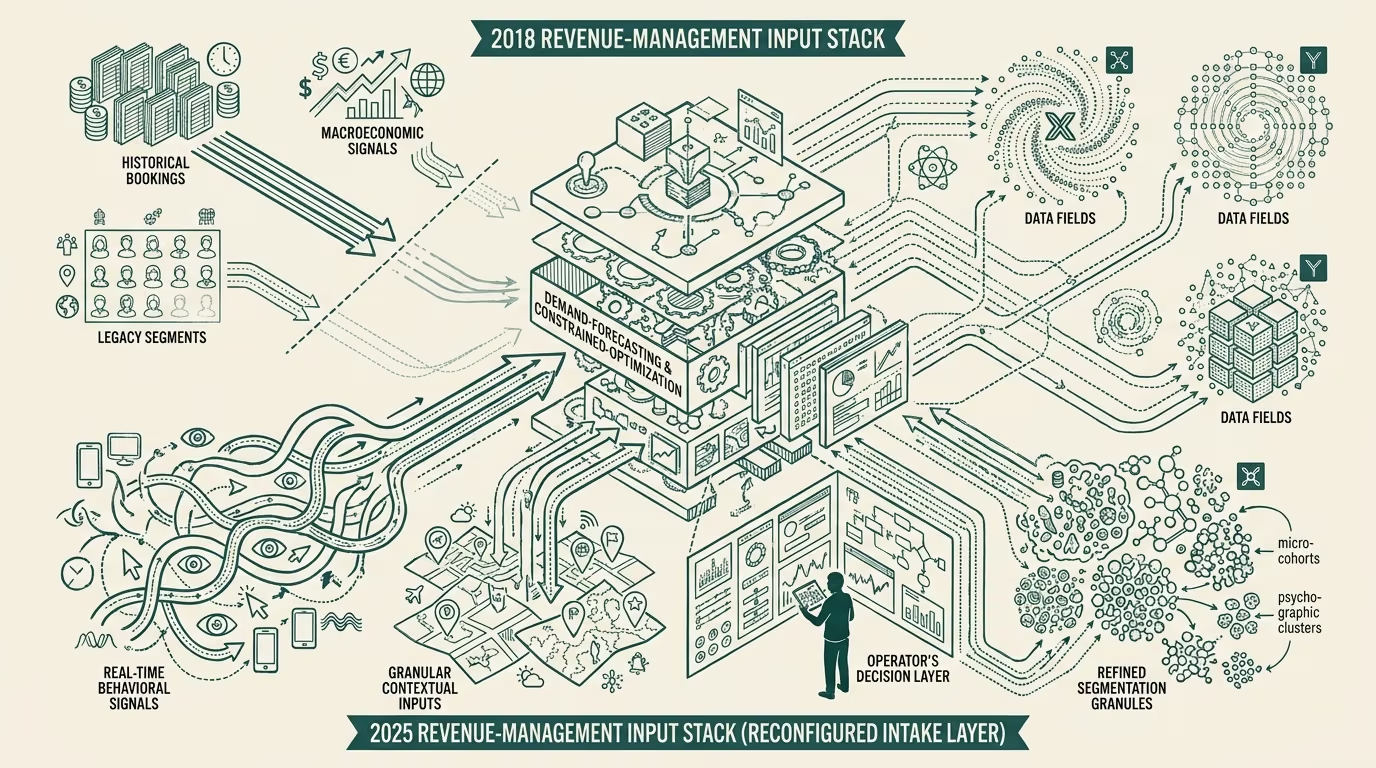

The 2018-2022 generation of revenue-management systems consumed roughly the same input set across the airline category and the hotel category. Historical bookings going back 5-7 years. Macro-economic indicators (GDP, unemployment, fuel cost, currency). Calendar features (day of week, month, holiday adjacencies). Competitor pricing scraped on a roughly daily cadence. Channel-level booking volume (direct, OTA-1, OTA-2, GDS). Loyalty-status-marker on the booking. Trip-shape (one-way / round-trip / multi-city; nights of stay; advance purchase window).

That set produced the demand forecast. The forecast fed an optimizer that ran constrained inventory-allocation decisions: how much of the cabin to leave open at each fare class for the days remaining to departure, how much to discount the corner-room category that historically went unsold by Friday, and so on. The pricing-decision was the optimizer's output. The architecture was demand-forecast + optimizer, calibrated against historical patterns.

What entered the input layer between 2022 and 2025 was a different shape of data. Five named additions, each with a different operator-grade implication.

First, real-time event-anchored demand signals. Every major destination has a calendar of events (sports, conferences, festivals, concerts) that drive demand spikes the historical-pattern forecaster captures only when the event is annual and fixed-date. Events that move year to year (Super Bowl in different cities, Olympic-class events, World Cup, climate-driven destination shifts) confuse the historical forecaster. The new input layer integrates event-calendar data licensed from event-aggregators (PredictHQ being the dominant vendor through this window) plus social-signal data that surfaces emerging demand-drivers (a viral TikTok about a particular hotel; a destination wedding cluster posted to Eventbrite; a late-add concert announcement). The forecast now flexes against events the historical pattern does not see.

Second, weather-adjusted demand. The 2018 forecaster knew it was June. The 2025 forecaster knows the 14-day forecast for the destination is showing an unusual heat-dome that will compress beach-season demand into a tighter window. The weather-adjusted demand layer requires both a high-resolution forecast feed (DTN, IBM-The-Weather-Company, AccuWeather Enterprise) and a model-side ingestion that translates forecast deviations into demand curves per destination. Hotels with outdoor amenities (beach resorts, ski properties) saw the largest forecast-improvement gains from this addition. Airlines saw smaller but real gains on weather-correlated routes.

Third, contextual personalization signals at the channel layer. The 2018 forecaster knew the booking came through OTA-1. The 2025 forecaster knows the user-cohort the OTA delivered, with what willingness-to-pay signals (return-visitor; mobile-app vs web; logged-in vs guest-checkout; cart-abandonment history). The channel-level segmentation that the OTAs always did internally is now exposed to the supply-side via richer booking metadata, and the supply-side revenue manager segments price against that. The change is not technical capability; the change is contractual: OTA-supplier data-sharing agreements through 2023-2024 expanded what the supplier sees.

Fourth, competitor-pricing at the granularity that matters. The 2018 forecaster scraped competitor-pricing daily. The 2025 forecaster ingests competitor-pricing at the 15-minute or 5-minute cadence with full-funnel signal (search-result-position, displayed-price, click-through-on-displayed-price). The data vendors here are Sojern, Onyx, Lighthouse, OTA Insight (now Lighthouse), and a handful of specialty vendors with airline focus. The granular competitor signal lets the model differentiate between a competitor's listed price and the price the competitor is actually achieving (which is often lower after promotions and cart-discounts). Pricing decisions get sharper when the comparison set is the actual achieved-price, not the listed-price.

Fifth, downstream-revenue signal. Hotels with food-and-beverage, spa, and resort-fee revenue and airlines with ancillary-revenue (seat selection, baggage, in-flight purchase) now feed the downstream-revenue layer back into the room-rate or fare-pricing decision. The 2025 forecaster optimizes for total-revenue-per-traveler, not just the nightly-rate or the fare. The implication is that a hotel willing to discount the nightly rate to a customer-cohort with high F&B spend can produce a better total-revenue outcome than a hotel pricing only on the nightly. This requires both the data integration (PMS to point-of-sale to F&B systems) and a multi-objective optimizer. Both have been steadily building out across the window.

These five input-layer additions are the actual story of the 2022-2025 RM evolution. The trade press writes about new AI architectures because architectures are legible. The operator class working with the systems sees the input layer as the thing that moved.

Section two: the segmentation refinements

What drops out of the new input layer is segmentation refinement. The 2018 system priced against perhaps a dozen named segments (corporate, leisure, group, packaged-tour, distressed-inventory, last-minute, advance-purchase, loyalty-tier-1 through tier-3, peak vs off-peak). The 2025 system prices against several hundred segments, generated dynamically from the input layer's joint distribution.

The named segments still exist as taxonomic anchors. The actual pricing decisions are made against the dynamic segments. A typical 2025 pricing decision might price against: "leisure traveler, mobile-app booking, 18-day-out advance purchase, weather-improving destination, neighbor-hotel-just-discounted, loyalty-tier-2, low-cart-abandonment-history." The segment is a join of seven inputs. The system has thousands of these. It does not need to name them; it just prices each one separately.

The segmentation refinement matters because it creates pricing-discrimination capacity that the 2018 system structurally lacked. A 2018 system charging a single price to all corporate-segment customers leaves money on the table compared to a 2025 system that prices the corporate-traveler-with-frequent-route-history-and-flexibility separately from the corporate-traveler-on-mandatory-policy-itinerary. The two travelers had the same 2018 segment. The 2025 segments differentiate them.

The refinement also creates a new operating-risk surface. Pricing-discrimination at the granularity the 2025 system supports is regulatory-class sensitive in a way the 2018 system was not. The U.S. DOT inquiries into airline algorithmic pricing in 2024-2025, the EU consumer-protection conversations around dynamic-pricing transparency, the FTC engagement with hotel surcharges, all sit downstream of the 2025-vintage pricing-discrimination capacity. The operator class running these systems has to think about both the revenue-capture upside and the regulatory-exposure surface, where the 2018-vintage operator could think largely about the upside.

Section three: the operator-class question of which inputs

If the input layer is the variable, the operator question is which inputs to feed the model. There are three sub-questions inside that.

License vs build vs capture. PredictHQ, DTN-class weather, Sojern-class competitor-pricing, the OTA channel-data feeds: these are licensed inputs from external vendors. Cost ranges from $50K/year for a single-vendor feed to several million for a bundled enterprise data stack. License-side decisions are about which inputs the model gets access to. Build-side decisions are inputs the operator generates internally (loyalty data, direct-channel booking data, downstream-revenue data, customer-history). Capture-side decisions are inputs the operator does not currently see but could capture through partnerships, integrations, or on-property data-collection (the wearable data of the spa-customer; the on-property browsing data; the partner-airline's booking data on connecting itineraries). Each of the three has different cost-and-control profiles.

Input bundling versus best-of-breed. A typical 2025 enterprise RM stack includes both the bundled vendor (one of the three or four full-stack RM vendors that ships with their own input feed) and a best-of-breed input layer the operator licenses separately and integrates. The bundled approach is simpler; the best-of-breed approach captures upside the bundled vendor's curated feed misses. Operators with the engineering capacity to build the integration layer go best-of-breed; operators without it stay bundled.

Input quality versus input quantity. More inputs are not always better. Each new input has integration cost, ongoing data-quality risk, and a marginal lift on forecast accuracy. The operator-tier question is which inputs lift the forecast in ways the existing inputs don't already cover. Weather signal, for example, is high-value for beach resorts and low-value for downtown business hotels in temperate climates. Event-calendar signal is high-value for sports-host-city hotels and low-value for airports. Operators picking inputs by industry-default (because the consultancy-class said weather signal matters) over-license; operators picking inputs by their own forecast-residual-analysis license tighter.

The under-discussed operator fact is that the input layer's lift is not uniform across the operator population. A single-property boutique hotel in a stable mid-tier city does not benefit much from a $250K/year event-calendar feed. A 200-property urban-hotel chain in event-heavy markets benefits tremendously. The operator-grade question is which inputs produce lift for this operator's specific demand-pattern.

Section four: what a pricing strategy looks like when inputs are the variable

A pricing strategy in 2018 was a model-and-architecture choice. The operator picked an RM vendor (IDeaS, Duetto, Atomize, in-house build) and the pricing strategy was largely the vendor's defaults plus the operator's overrides on a small number of business-rule parameters.

A pricing strategy in 2025 is an inputs-and-segmentation choice. The operator picks the input layer (which licensed feeds, which internal data sources, which capture programs), the segmentation depth (how many dynamic segments the system prices against, with what regulatory-class governance), and the multi-objective optimization weights (how to balance nightly-rate-revenue against ancillary-revenue against loyalty-program-impact against regulatory-exposure-risk). The vendor's model-class is now downstream of these decisions.

For an operator founder building in this space (a new RM vendor, an input-feed startup, a segmentation-quality tooling provider) the durable read is that the value capture has migrated from the model layer to the input layer and the segmentation layer. The operator-tier buyer is no longer asking which model is best; the operator buyer is asking which inputs do you give me access to and how do you help me segment against them. Founders pitching against the wrong frame (look at our model architecture) get a polite hearing and no purchase order. Founders pitching against the right frame (here are five inputs you do not currently have, calibrated for your operator profile) close.

The 2022-2025 inflection is clear in retrospect. The model architectures that won are the ones that integrated the new input layer cleanly. The inputs that won are the ones that produced lift on demand-pattern segments the existing forecaster missed. The pricing-strategy decisions that won are the ones that picked inputs by residual-analysis rather than by industry-default. The category through 2025-2028 will continue to compound on this trajectory; the operators who get the input-layer reframe are running ahead of the operators still treating the model as the variable.

Revenue management is now an inputs problem. The architecture stopped being the variable about three years ago. Operators who recognized that ship better systems; operators who didn't are still running the wrong evaluation criteria when they pick a vendor.

—TJ