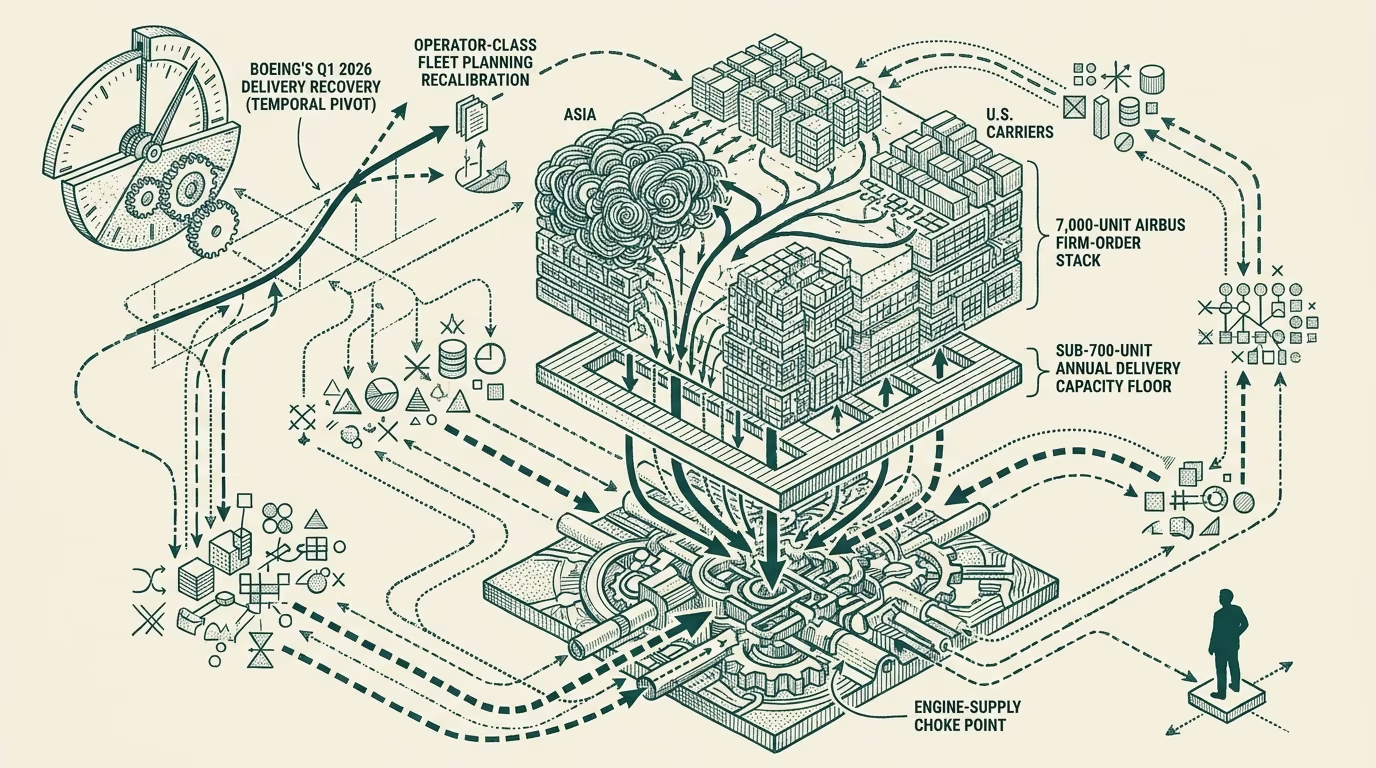

Airbus narrowbody backlog math, updated: Boeing's Q1 2026 delivery beat changed the calculus.

The Airbus A320/A321 narrowbody backlog at the end of 2025 stood at roughly 7,000 firm orders against an annual delivery capacity that has been running below 700 units for the past three years. The implied backlog-to-deliveries ratio sat above ten years for most of 2024-2025, which is the kind of order-book overhang the commercial-aviation category has not seen in any prior cycle. Boeing's parallel narrowbody backlog was structurally similar in shape but constrained by the production-rate problems the company has been working through since 2024.

The Boeing Q1 2026 delivery recovery, where the company beat its own delivery guidance for the quarter and signaled a credible 737 MAX production-rate trajectory through 2026, changed the operator-class calculus on the narrowbody-fleet planning question. This is a tight numbers piece on what the recalibration looks like, where the constraint actually sits, and what carriers waiting on the order book should reasonably be planning against.

What the Airbus backlog math actually shows

The end-of-2025 firm-order book at Airbus for the A320/A321 family covered approximately 7,000 units, with the geographic distribution running heavily toward Asian carriers (the long-haul-low-cost expansion) and U.S. carriers (the post-COVID fleet refresh and capacity expansion). The book-to-bill ratio across 2024-2025 ran consistently above 1, with new orders accumulating faster than the company could deliver against the existing book. The backlog grew through both years.

Delivery delays for new orders placed in 2024 ranged from 8 to 12 years, depending on the type and the carrier-position in the order queue. Carriers placing fresh orders in 2025-2026 are looking at delivery slots in the 2034-2038 range. The structural read is that the carriers placing orders today are placing them for a fleet they will operate in their next-business-cycle planning window, not the current one.

The delivery delays compound for carriers that are growing their fleet at the same time as they are refreshing aging aircraft retiring out. The carriers running this dual constraint have been forced into the secondhand-aircraft market, the leasing-market for transitional capacity, and selective deferral of fleet-refresh decisions that they would have preferred to act on sooner. The order-book overhang is not just a manufacturer problem; it is a carrier-side fleet-planning problem.

The engine-supply choke point

The structural choke point in the Airbus backlog through 2024-2025 has been engine supply, specifically the CFM LEAP and Pratt and Whitney PW1100G geared-turbofan engine families that power most of the A320neo / A321neo production. CFM (the GE-Safran joint venture) has run production-rate constraints driven by hot-section component supply, with the fan-and-compressor blade machining capacity being the tightest single constraint. Pratt and Whitney's PW1100G has run separate constraints driven by the powdered-metal contamination issue that surfaced in 2023 and has required substantial in-service inspection-and-replacement work that has pulled engineering capacity away from new-engine production.

The combined effect is that engine availability has been the binding constraint on Airbus's narrowbody delivery capacity for most of 2024-2025. The airframer can build airframes faster than the engine partners can deliver engines. The order-book delivery dates reflect the engine-supply trajectory, not the airframe-production capacity.

Through Q4 2025 and into Q1 2026 the engine-supply picture has shown some improvement. CFM's LEAP production has been ramping toward higher rates as the hot-section capacity expansion has come online. Pratt has been working through the in-service fleet's PW1100G remediation while ramping new-engine production, with the latter showing improvement through the second half of 2025. The 2026 delivery rate at Airbus is forecast to recover toward 750-800 units annually, with further growth through 2027 if the engine-supply trajectory holds.

What Boeing's Q1 2026 delivery beat changed

The Boeing Q1 2026 delivery recovery had two effects on the Airbus narrowbody calculus, neither of them captured well in the trade-press coverage that read the recovery as primarily a Boeing story.

The first effect is on the carrier-fleet-planning question. Carriers running narrowbody fleet decisions through 2024-2025 had been planning against a Boeing constraint that limited their realistic narrowbody options to the Airbus side. With Boeing back as a credible delivery-capable competitor through 2026 and beyond, the carriers' choice set widens. Some carriers that had been queuing additional A320/A321 orders are reconsidering whether to split the order between the two manufacturers, which moderates the new-order pressure on the Airbus book. Others are evaluating whether to pivot the narrowbody strategy entirely to Boeing for the next refresh cycle, which would produce more substantial moderation.

The second effect is on the engine-partner allocation question. The CFM LEAP engine powers both the A320/A321neo and the 737 MAX. CFM's production capacity is shared across the two airframer customers, with the allocation between them determined by the airframers' production rates and the contractual structures behind the engine deliveries. Boeing's higher production rate in 2026 will draw a higher share of CFM's output toward Boeing aircraft, which means the engine-supply constraint on Airbus's narrowbody production is structurally tighter even as CFM's overall output grows. This is the part of the picture the trade-press has been generally not running.

The combined effect is that the Airbus narrowbody backlog is unlikely to clear at the rate the engine-supply-improvement trajectory alone would suggest, because the engine-supply allocation will favor the airframer with the higher production rate. Carriers planning against the Airbus delivery trajectory should price the slower-clearing scenario into their fleet plans.

What this leaves the operator class with

For carriers running narrowbody fleet decisions in 2026-2027, the operator-tier read is that the dual-supplier sourcing posture (orders split between Airbus and Boeing) is more structurally available than it was through 2024-2025, with both manufacturers in the credible-delivery range for the medium-term planning horizon. Carriers that have been single-sourced on Airbus through the Boeing-constrained period should evaluate whether the dual-source flexibility is worth pursuing for the next order cohort.

For carriers that have already placed Airbus orders for 2027-2030 delivery, the durable read is that the delivery dates are likely to hold or improve modestly relative to the 2024-2025 worst-case scenarios, with engine supply continuing to be the binding constraint and the CFM-allocation dynamic compressing the upside.

For Airbus, the durable read is that the backlog overhang is durable through 2027-2028 and likely beyond, with the company's leverage on the carrier-class buyer remaining substantial. Airbus's pricing power on new orders, which has been strong through the Boeing-constrained period, may moderate as the dual-supplier dynamic returns, but the production-capacity constraint protects the company from substantial pricing erosion in the near term.

For investors evaluating the commercial-aviation manufacturer category, the read is that the Airbus narrowbody franchise is structurally durable and the order-book overhang protects the revenue trajectory through the medium term, while the Boeing recovery improves the duopoly's overall capacity utilization and reduces the airframer-side risk that had been priced into the category through 2024-2025.

The Airbus backlog math in early 2026 is more nuanced than the headline backlog-to-deliveries ratio suggests. The engine-supply allocation, the Boeing recovery, the carrier-side dual-sourcing dynamics, and the longer-cycle fleet-planning rebalancing all interact in ways that the simple backlog-overhang framing does not capture. Operators reading the math carefully are positioning for the medium-term scenario where the constraint moderates without disappearing. Operators reading the headline are positioning for a constraint scenario that is partly already past.

—TJ