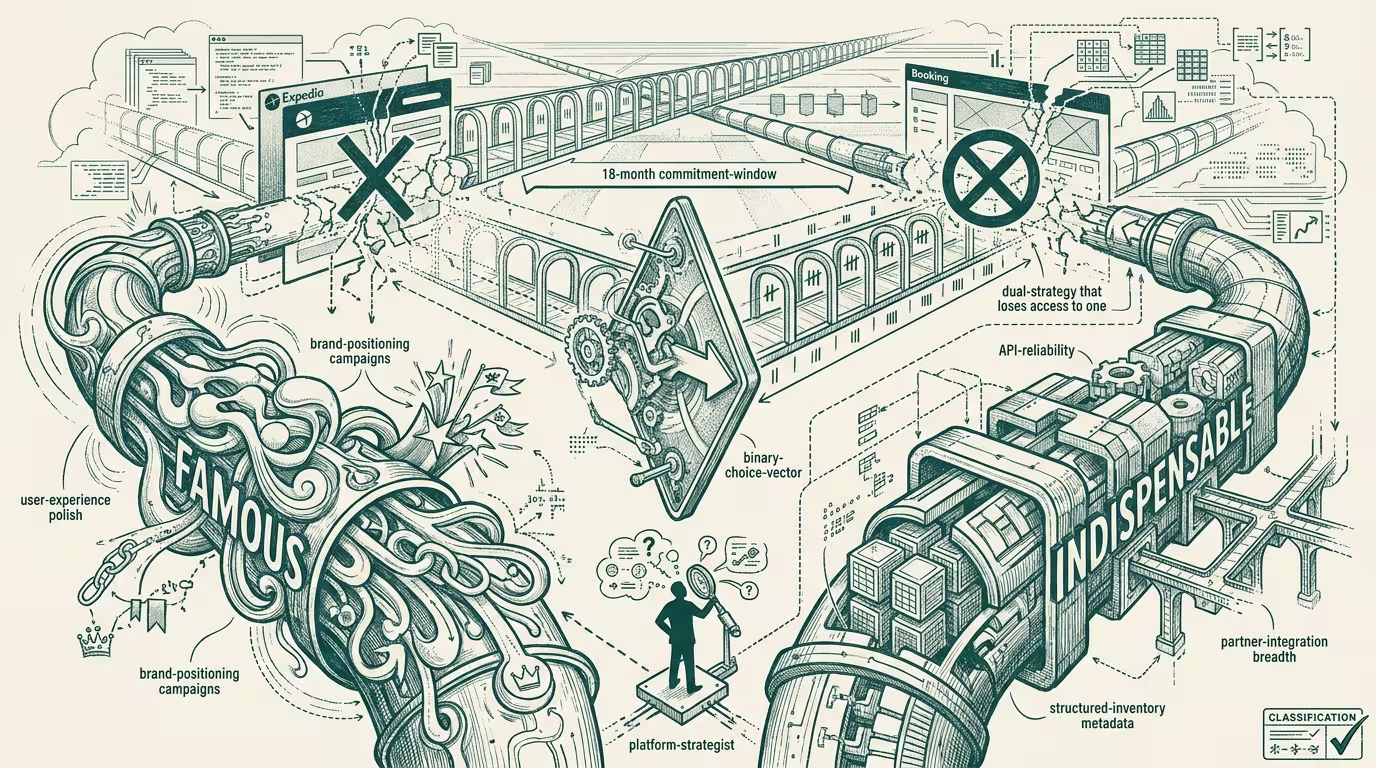

Famous or indispensable. Travel platforms have to pick one.

Skift founder Rafat Ali published an essay sequence through Q4 2025 and into Q1 2026 articulating a binary strategic choice for OTAs: be a consumer brand (famous) or be invisible infrastructure (indispensable). The framing landed because it named the structural problem agentic AI creates for the dual-business diversification that built Booking and Expedia.

The dual-business model that worked through 2024 was: own the consumer-facing brand for direct customer acquisition, and run B2B infrastructure (inventory APIs, search APIs, white-label distribution) for partner integration. Each side of the business reinforced the other. The brand drove direct traffic; the infrastructure captured indirect distribution; the combination produced asymmetric scale economics.

In an agentic-AI environment where ChatGPT Agent Mode, Claude's task agents, and Gemini's travel-planning surfaces book directly, the dual-business model breaks. Agents bypass the consumer-brand layer and plug into the inventory infrastructure directly. The platform that runs both sides has to choose which side it's optimizing for, because the optimizations are now operationally incompatible.

_Famous or indispensable. The platform that tries to keep both seats loses access to one or the other._

Compare the two strategies side by side and the optimization conflict surfaces. Optimizing for consumer-brand value requires investments in user-experience polish, brand-positioning campaigns, customer-loyalty programs, and the conversion-funnel work that turns brand-awareness into bookings. Optimizing for indispensable-infrastructure value requires investments in API reliability, structured-inventory metadata depth, partner-integration breadth, and the back-end work that makes the platform the AI's preferred-rail for booking-completion. The investments compete for the same capital and operate against different KPIs. A platform with finite capital allocates against one strategy or the other. The platform that allocates against both produces inferior outcomes on both metrics.

What does the timeline look like at the operator level? Binary at the strategy level and 18 months at the commitment-window. Operators in the OTA category have to make the choice explicitly through 2026 and execute against it through 2027. Booking is, in operating terms, partway down the indispensable path through deeper inventory licensing arrangements (Vrbo integrations, the supply-side partnerships) but is also defending a consumer-brand position that the indispensable strategy will compress. Expedia is partway down the consumer-brand path through Vrbo and the Hotels.com brand portfolio but is also running infrastructure investments. Both companies are running the dual strategy. By Q4 2026 both will have to commit. The companies that commit early capture the optimization-class advantage; the companies that commit late absorb the indecision cost.

What does each strategy actually require? The famous strategy continues the existing playbook with more aggressive consumer-brand investment. The indispensable strategy requires a fundamental operating-model shift — the company becomes a B2B-infrastructure provider whose primary customers are AI surfaces and partner platforms rather than end consumers. The shift includes pricing-model changes (API-class pricing rather than booking-fee-class), customer-relationship changes (partner-account-management rather than consumer-marketing), and revenue-recognition changes (recurring-API-revenue rather than transactional-booking-revenue). Operators choosing indispensable have to absorb the operating-model shift. Operators choosing famous don't.

What does the ceiling on each look like? The famous strategy has lower operator-class returns at scale than the indispensable strategy. The consumer-brand layer in agentic-travel commerce is a smaller market opportunity than the infrastructure-rail layer because the brand layer is bypassable by the agent. The infrastructure layer is not bypassable — every booking, agent-mediated or otherwise, has to flow through some inventory-and-payment infrastructure. Operators who can become the infrastructure of choice capture rents from every booking the agent class generates. Operators competing for the residual consumer-direct booking volume are competing for a shrinking share of total travel-commerce volume. The famous strategy is, in operating terms, the lower-ceiling strategy.

The same shape recurs across categories where agentic AI is bypassing consumer-brand layers. E-commerce platforms (Amazon's various sub-categories vs. the long tail of brand-direct platforms), financial-services platforms (consumer banking vs. infrastructure-rails like Plaid and Stripe), software platforms (consumer SaaS vs. infrastructure SaaS like AWS-class and Snowflake-class). Each category has its own version of the binary choice and its own 18-24 month operator-tier commitment window.

What survives all of this is that the Skift framing is one of the cleaner Q4 2025-Q1 2026 articulations of the strategic choice OTAs face, the binary nature of the choice is operationally durable, and the operator discipline is to make the choice explicitly within the 18-month window. Operators with explicit famous strategies are positioned to capture consumer-brand-class value as it gets compressed. Operators with explicit indispensable strategies are positioned to capture infrastructure-class value as it expands. Operators running both strategies are absorbing the optimization conflict and producing inferior outcomes on both metrics.

Famous or indispensable. The travel platforms have to pick one. The platforms that pick are operating-coherent in either direction. The platforms that try to keep both seats are operating-incoherent and will lose access to one of the two within the 18-month window the agentic-AI shift is collapsing.

—TJ