The hospital-at-home pilot data, four years in.

The hospital-at-home waiver was supposed to end with the public-health emergency. It did not.

CMS extended the waiver authority twice, most recently through the end of 2026, and the extension has been treated inside the participating health systems as a quasi-permanent feature of the regulatory landscape since the second extension landed. The pilot phase has been over for some time. The data exists. The systems that leaned into hospital-at-home across 2022 through 2025 did so with operational evidence in hand rather than the speculative case the early advocates were making in 2021 and 2022.

Six notes on what the evidence says, looking back from March 2026.

The savings are real but the headline number was wrong

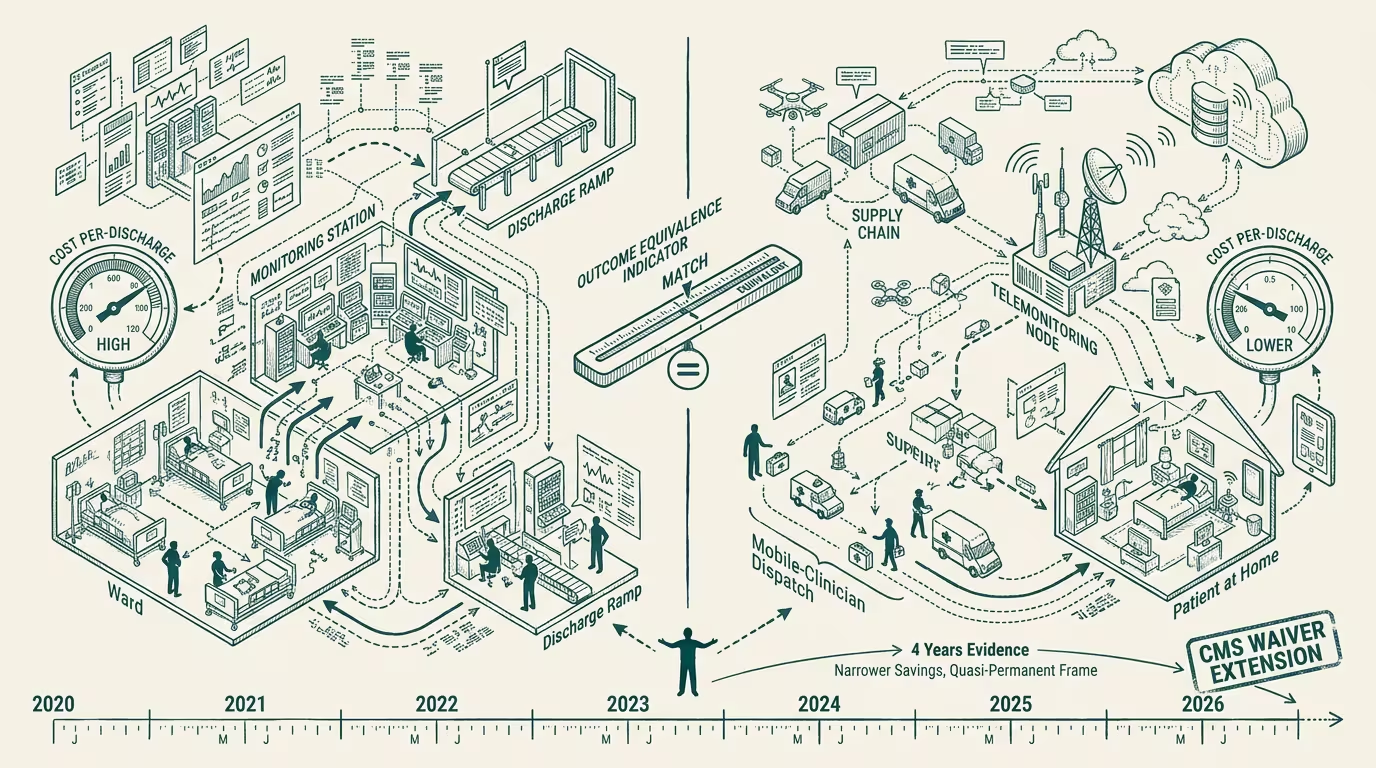

The 2021 advocacy case for hospital-at-home leaned on a thirty-percent cost reduction figure that came out of the early Mount Sinai and Brigham programs. The figure was a real number from a real cohort. It was also selected for the kind of patient who could be safely managed at home with the kind of staffing model those programs had built, and the rest of the system inferred a much broader savings claim from a much narrower data point.

Four years of broader implementation has produced a more honest range. The cleanest published numbers from the second cohort of programs, which include the Atrium, Cleveland Clinic, and several of the Texas systems, settle around fifteen to twenty-two percent total cost reduction against a matched in-hospital cohort. That is still a real number. It is not the thirty-percent figure that anchored the early commentary, and the gap between the two has been quietly absorbed by the field rather than re-litigated. That is the wrong way to handle a corrected estimate.

The reason the headline number compressed is that the pilot programs cherry-picked the patient population. Patients with reliable home environments, supportive caregivers, mid-acuity diagnoses, and short expected lengths of stay were the patients who got referred to the program. As programs scaled, the pool widened, and the marginal patient in the broader pool generated less savings than the marginal patient in the pilot pool. This is a generic feature of pilot-to-scale transitions in healthcare, not a flaw of hospital-at-home specifically, but the field tends to forget the lesson and write each new program's pilot results as if they will hold at scale. They will not, ever, anywhere.

The outcomes are the strong part of the case

Where the data has been more robust than the cost case is on the outcomes side. Mortality, thirty-day readmission, and patient-reported quality-of-life scores have held even or modestly favored the hospital-at-home arm in the better-designed studies. The mechanism is plausibly that home environments produce less hospital-acquired infection, less delirium in older patients, and better sleep, all of which are real determinants of outcome that the in-hospital setting has been slow to address. The studies that show outcome equivalence are the ones that have been replicated across systems, and the replication is where the operational confidence comes from. The cost claim has been revised down. The outcomes claim has been confirmed. The advocacy case should pivot accordingly. It mostly has not.

There is a subtler point inside the outcomes data that the operator should hold onto. The patient population eligible for hospital-at-home, even in the wider second-cohort pool, is a population where the marginal hour of in-hospital monitoring is producing relatively little outcome value. The patients for whom in-hospital monitoring is doing the most work — the unstable post-operative patients, the high-acuity infections, the patients who need procedural intervention on a few hours' notice — were never candidates for hospital-at-home and still are not. The outcome equivalence is a real finding _within the eligible population_. It is not a claim that any patient anywhere is just as well off at home, and the operator who treats it as such is going to push the eligibility criteria past the safety frontier and produce the case that gets used in court to roll the program back.

The labor-arbitrage worry did not materialize

In 2022 the loudest objection to hospital-at-home was that it would be a vehicle for converting unionized hospital nursing labor into lower-paid home-health labor under a different staffing model. This was not a hypothetical worry; the precedents in long-term care and home dialysis are real, and the union response in those categories was instructive. It did not happen with hospital-at-home, and the reason is interesting. The labor model that the most successful programs converged on uses the same hospital nursing pool, on the hospital payroll, rotating between in-hospital shifts and hospital-at-home shifts in a single job classification. The home visits are conducted by the same nurses who would have provided in-hospital care, and the technology layer (remote monitoring, video rounds, paramedic dispatch for emergent in-person needs) supplements rather than displaces the nursing role.

Two factors locked this in. First, the early reimbursement structure required the hospital-at-home patient be under direct attending-physician care from a hospital-affiliated medical group, which made it operationally difficult to subcontract the nursing layer to a separate home-health agency without re-architecting the chain of accountability. Second, the nursing unions in the systems that piloted aggressively (Mass General, the Atrium system, Mount Sinai) negotiated jurisdictional clauses that pulled hospital-at-home explicitly inside the existing contract. The combination meant the labor-arbitrage path was closed before it could be opened. The systems that came into hospital-at-home across 2024 and 2025 inherited this norm and found it expensive to deviate from it. The labor-arbitrage worry should be retired from the commentary.

The technology stack is more conservative than the marketing implies

The remote-monitoring vendors selling into hospital-at-home programs ship pitch decks that imply a sophisticated stack of continuous biometric monitoring, machine-learning-driven deterioration detection, and predictive intervention. The deployed reality is much more modest. Most programs are running a small set of vital-sign monitors (blood pressure, pulse, oxygen saturation, temperature) on roughly four-to-six-hour cadence, with a video-call rounding tablet, a paramedic dispatch contract for emergent needs, and a nursing call-center that triages alerts. The continuous-biometric layer exists as an option on most platforms but is rarely turned on, partly because the alert rate would overwhelm the call center and partly because the false-positive rate on the deterioration models is still too high to trust at scale. The deterioration-prediction models will improve, and at some point will be operationally useful. The 2022 through 2026 window was not that point.

This conservatism is, on close reading, the right call. The clinically eligible population is by construction the population where deterioration is unlikely, and a high-sensitivity monitoring layer would produce a high rate of unactionable alerts. The systems that captured the 2024 through 2025 phase of hospital-at-home growth were not the systems with the most ML. They were the systems with the cleanest workflow integration and the fastest paramedic-dispatch latency in their delivery footprint.

The technology bottleneck is logistics, not algorithms.

The eligibility frontier is where the next decision sits

The expansion path that has the most attractive economics, and also the most uncomfortable safety implications, is widening the eligibility criteria to include moderate-acuity post-operative patients and selected high-acuity infectious-disease patients. The savings on these populations would be larger; the outcome data is much thinner; the failure-mode profile is qualitatively different from the failure-mode profile of the current eligible population. The operator decision across 2024 and 2025 was not whether to expand eligibility — every program faced commercial pressure to do so — but how to construct an evidence path that would not produce the case that gets used to shut the program down.

The right shape of an evidence path is staged eligibility expansion with a pre-registered protocol, randomization where it is operationally feasible, blind outcome adjudication, and pre-committed stopping rules. The wrong shape is opportunistic expansion driven by the volume that happens to be in the door that month. The systems that picked the wrong shape are the systems whose programs get unwound when the first bad outcome lands in the press, and the entire field gets set back two to three years. This is a coordination problem that the field has handled poorly in adjacent areas (early ICU telemedicine, early in-home dialysis), and there is no reason to think hospital-at-home will handle it better unless the systems that have the most to lose actively coordinate on a stricter expansion protocol than the marginal economics would dictate.

There is a related point, less appreciated inside the US conversation than it should be, about how the international comparison shifts the eligibility argument. Australia, the Netherlands, Spain, and parts of Italy have run hospital-at-home programs for two decades, on different reimbursement architectures, and the eligible-population definitions in those programs are noticeably wider than the US definitions are now. The wider eligibility was not the result of a more aggressive cost calculus; it was the result of a less aggressive one, in systems where the in-hospital alternative was less expensive, less profitable to the institution, and less subject to the labor and litigation pressures that shape the US calculation. The Australian program, in particular, has run with a moderate-acuity post-operative population for over a decade with outcomes that are at least equivalent to the in-hospital arm. The US operator commentary tends to treat that evidence as not quite portable, on the argument that the regulatory environment, the malpractice environment, and the patient-population characteristics are different enough that the international evidence does not constrain the US decision. The argument is true but it is being used to dismiss evidence that should be informing the design of the US expansion path. The US programs that handle the eligibility frontier well treat the international evidence as a lower-bound argument: the patients who do well at home in Australia are the patients who will do well at home in the US, and the structural reasons the US system has been slower to expand are reasons about institutions, not reasons about clinical outcomes. The systems that internalize that distinction are the systems that get the expansion right. The systems that do not use the international evidence selectively, only when it supports a position the program leadership had already adopted, which is the standard institutional response to inconvenient external data and the response that produces the slowest progress on the eligibility frontier.

The CMS extension is doing more work than the operators are crediting

The waiver extension through 2026 is being treated inside the participating systems as a temporary breathing room. It is more than that. The extension is, in practical terms, the policy bridge between the pandemic-era authorization and a permanent CMS payment category for hospital-at-home, and the comments and rulemaking activity in motion suggest the permanent category will land in the 2026 or 2027 rule cycle. The operator move is to plan for the permanent category, not the next extension. Programs that are still running on the assumption that the model is temporary are under-investing in the operational infrastructure that the permanent category will reward, and they will be at a disadvantage when the rule lands and the payment terms favor the systems that have built the workflow integration, the paramedic dispatch network, and the staffing rotation rather than the systems that have been waiting to see if the program persists.

The systems that are over-investing right now look paranoid about return-on-investment. They will look prescient in eighteen months. The systems that are under-investing look disciplined right now. They will look slow in eighteen months.

The data is sufficient to make the call. The CMS signal is sufficient to underwrite it. The field bifurcates on this decision, and the bifurcation shows up in operating margins.

The summary is that the pilot phase produced a real but smaller-than-claimed cost saving, an outcome equivalence that has held up under replication, a labor model that closed off the worst-case scenario the early objectors warned about, a technology stack that is more conservative and probably better-calibrated than the marketing suggests, and an eligibility frontier that remains the next major decision point. The CMS extension is the policy signal that the model is becoming permanent. The operators reading it as temporary are misreading the signal. The 2024 through 2025 window was the decision window, and the systems that picked the right operating posture in that window are positioned to compound advantage against the systems that picked the wrong one.

—TJ