Long-stay travelers are an unbuilt platform tier.

By early 2025 there are 70+ countries running digital-nomad visa programs, each with different income thresholds, different tax treatment, different durations, different proof-of-employment requirements, and different renewal-process timelines. Portugal's D7. Spain's digital nomad visa. Estonia's e-Residency-plus-visa. Mexico's Temporary Resident card with the right paperwork. Bali's B211A and the longer pathway. Croatia. Costa Rica. Greece. The list compounds.

The cohort using the visas is small (low six figures globally, by the most generous estimate) but high-LTV in ways the existing travel category does not capture.

A long-stay traveler on a digital-nomad visa books accommodation for 30-90 days at a time, not 3-7 days. Their per-stay revenue is multiples of a typical leisure traveler's per-stay revenue. Their churn is annual rather than per-trip. Their willingness-to-pay for ongoing-relationship services (visa compliance, tax filing, banking, healthcare, address-of-record, package handling) is high because they cannot get those services from the home-country vendors that traditional travelers fall back on. The cohort is, in operating economics, a different kind of customer.

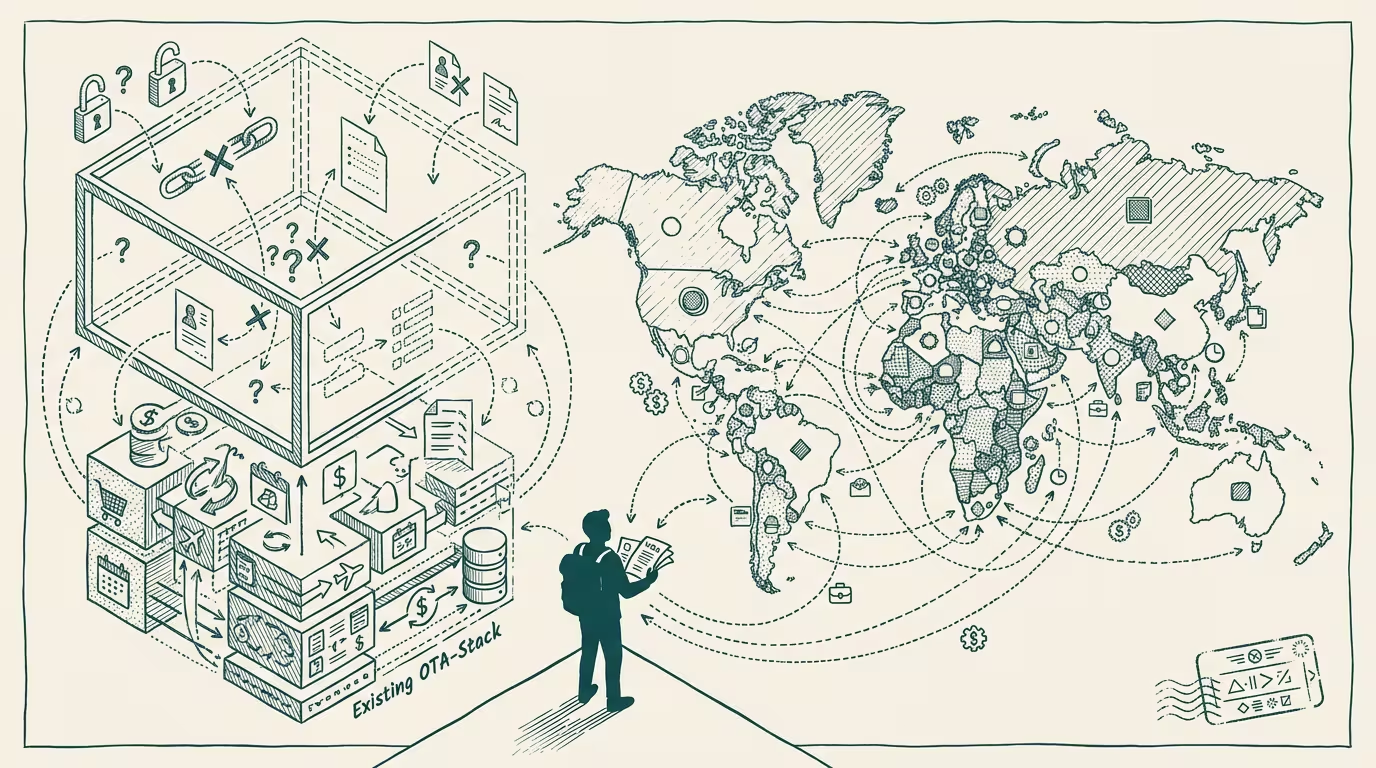

The OTA category does not serve this customer. OTAs optimize for transactions. The booking is the unit of value. The relationship after the booking is, in operating practice, a customer-service ticket and a review prompt. None of that maps to what a long-stay traveler needs.

What's actually unbuilt is the relationship-infrastructure layer. The platform that handles the compliance complexity (visa applications, renewals, tax-residency clarification across multiple jurisdictions), the ongoing services (banking with international fee structures, address-of-record, healthcare for the long-stay window), and the discovery layer (which destination's visa terms map to my income, my profession, my dependents, my chronic medical conditions, my pet). All three are services. None of them are bookings.

Why hasn't anyone built it? The cohort is small enough that the unit-economics math feels unconvincing at the deck level. A platform that serves 100,000 long-stay travelers globally at $2,000-5,000/year per customer is a $200M-500M revenue category. That number is large enough to be a real business and small enough that traditional travel-platform investors price it as a niche. The mismatch is why nobody has built it.

The regulatory complexity is real and discourages the platform-build on its own terms. A platform that handles visa compliance for 70+ countries needs legal and regulatory expertise across 70+ jurisdictions. The cost of acquiring that expertise is a meaningful chunk of the platform's first three years. Most platform-builders look at the cost and decide to build something else.

The cohort itself is fragmented across product categories the platform layer can't easily aggregate. Some long-stay travelers are remote employees (their employer handles compliance). Some are independent contractors (they handle compliance). Some are retirees (different residency rules). Some are entrepreneurs running businesses across multiple jurisdictions (the most complex case). The product that serves all four is structurally hard to design.

So the interesting bet is which adjacent category gets to it first. The candidates: the tax-services-for-expats category (Greenback Tax, Bright!Tax) extending upward into compliance-broader services. The international-banking category (Wise, Revolut) extending into residency-and-compliance. The remote-employer category (Deel, Remote.com) extending from employer-of-record into traveler-of-record. The traditional travel category (Airbnb, Booking) extending from short-stay into long-stay relationship infrastructure.

The remote-employer category has the best structural position. Deel and Remote.com already handle multi-jurisdiction compliance for the employer side. Extending to handle the employee-traveler's personal compliance is a smaller leap than the other adjacencies. Whichever of them ships the long-stay-traveler product first captures the category. By 2027 it's a $1B+ ARR business. By 2030 it's a multi-billion-dollar platform that the rest of the travel category has to integrate with rather than compete against.

The healthcare adjacency lands on the same gap. Long-stay travelers need healthcare across jurisdictions. The cohort's healthcare-access pattern is structurally different from either the home-country-employer-insured pattern or the country-of-residence-public-system pattern. The healthtech operator that builds the long-stay-traveler healthcare layer (subscription health insurance valid across the cohort's jurisdictions, telemedicine that respects local prescribing, in-country emergency-care relationships) builds into the same gap. That product also doesn't exist.

What's actually happening here is that there's a high-LTV cohort the existing platform layer is structurally not serving, the compliance complexity that has discouraged the build is decreasing as the regulatory frameworks mature, and the adjacent categories with the best structural position are not yet moving on it. The platform-tier company is, in operating terms, a 2026-2028 company someone is going to build, and the category will support it.

Long-stay travelers are an unbuilt platform tier. The build is operationally hard and structurally lucrative. The operator who recognizes the gap in 2025 is the operator running the category in 2030. The rest are competing on transaction-flow against a cohort that isn't actually transactional.

—TJ