Sick care doesn't become healthcare without a longitudinal data holder.

a16z's Big Ideas 2025 essay frames the next decade of healthcare as a shift from "sick care" (treat the disease that already presented) to "healthcare" (intervene earlier, prevent the disease from presenting at all). The framing is operator-class plausible. The economic model the framing implies is structurally different from the model the U.S. healthcare system has been running for sixty years.

What changes is who pays, who buys, and on what timeline.

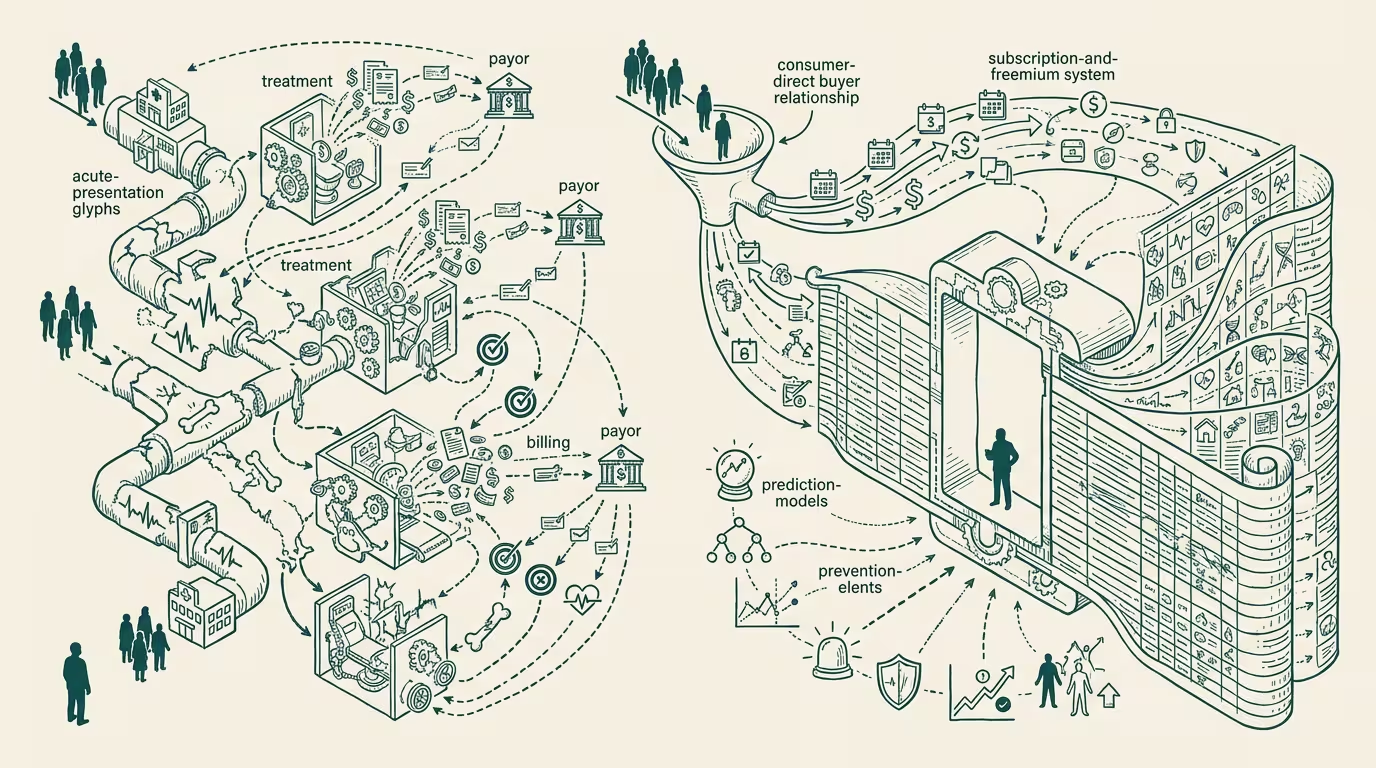

Sick care runs on episodic-claims economics. The patient presents with a problem, the clinician treats it, the payer reimburses on the claim. The buyer is the payer. The cycle time is episodic. The economic primitive is the claim.

Healthcare-in-the-shifted-frame runs on subscription-or-freemium economics. The patient pays continuously for ongoing intervention (longevity products, preventive monitoring, behavioral coaching, wellness platforms). The buyer is the consumer. The cycle time is continuous. The economic primitive is the subscription.

What's the load-bearing condition for the shift? A longitudinal data holder. A preventive intervention requires longitudinal data on the patient's baseline, their risk profile, their behavioral patterns, their response to the intervention. None of that is captured by the episodic-claim apparatus. The system that pays for "treat the cardiac event" does not know the patient's baseline cardiovascular trajectory. The system that pays for "treat the diabetic crisis" does not know the patient's three-year glucose-and-behavior trend. The longitudinal data holder is the entity that bridges between the two economic models, because the longitudinal data is the input both the consumer-paid-preventive and the payer-paid-treatment products need.

Who are the candidates? The wearables stack (Apple Watch, Whoop, Oura, Levels) holds the consumer-side longitudinal data. The pharmacy-platform layer (the GLP-1 platforms, the Shoppers Drug Mart pharmacy clinic format, the digital-health-platforms with adherence data) holds the consumer-paid intervention layer. The EHR vendor (Epic, Cerner) holds the clinical-encounter layer but not the consumer-side longitudinal data. The payer (UnitedHealth, Cigna, Aetna) holds the claims data but not the behavioral data. The pharma manufacturer holds the molecule but not the longitudinal-response data. None currently hold the full longitudinal data graph the shift needs. The party that gets to it first captures the next platform-tier of healthcare.

What has to converge for the shift to happen at scale? Three things, in sequence.

The consumer's willingness to pay for preventive products has to be larger than the consumer-product economics currently capture. GLP-1 platforms at $300/month suggest the willingness exists for some interventions. Wearables-as-subscriptions at $200-400/year suggest it exists at the monitoring layer. The harder question is whether the consumer pays for the integrated longitudinal product (continuous monitoring + behavioral coaching + preventive intervention) at the price the integrated product needs to charge to be viable. That number, on the available evidence, is roughly $1,000-2,000 per year per consumer for the integrated subscription. Some fraction of the population pays it. Most do not.

The longitudinal data graph has to be portable across the consumer's product choices. The consumer who switches from Whoop to Oura wants their data history to follow. The consumer who adds the GLP-1 platform wants the wearable data to inform the platform's adherence intervention. The data-portability infrastructure does not, in late 2024, exist at the level the integrated product needs. The party that builds it is, structurally, the platform that captures the next decade.

The regulatory frame has to allow the data to move. HIPAA in the U.S. and GDPR in the EU were calibrated for the episodic-claims era. The longitudinal data holder operates on a different legal frame because the consumer-paid relationship sits outside the traditional HIPAA-covered-entity scope. The regulatory frame is going to have to extend, and the extension will land in 2026-2028 with prejudice toward the data-holder that pre-built the consent layer.

What does this mean for healthtech founders in late 2024? Ask which side of this convergence the company is on. Companies whose product is one slice (a wearable, a GLP-1 platform, a behavioral-coaching app) without a strategy for the integrated longitudinal product are companies whose 2027 strategic position is being decided by whichever platform absorbs them. Companies whose product is _the longitudinal-data integration layer_ are the platform-tier candidates. The middle position — single-slice companies pretending to be platforms — is the worst position.

a16z is right that sick care to healthcare is the structural shift. The shift cannot happen without a longitudinal data holder. The candidates are moving. The party that builds the data-holder layer is the one that wins the next decade.

Sick care doesn't become healthcare without it. The capital flowing into 2025 will, on the available evidence, find this layer late and price the winner at a premium the early operators won't have to pay.

—TJ