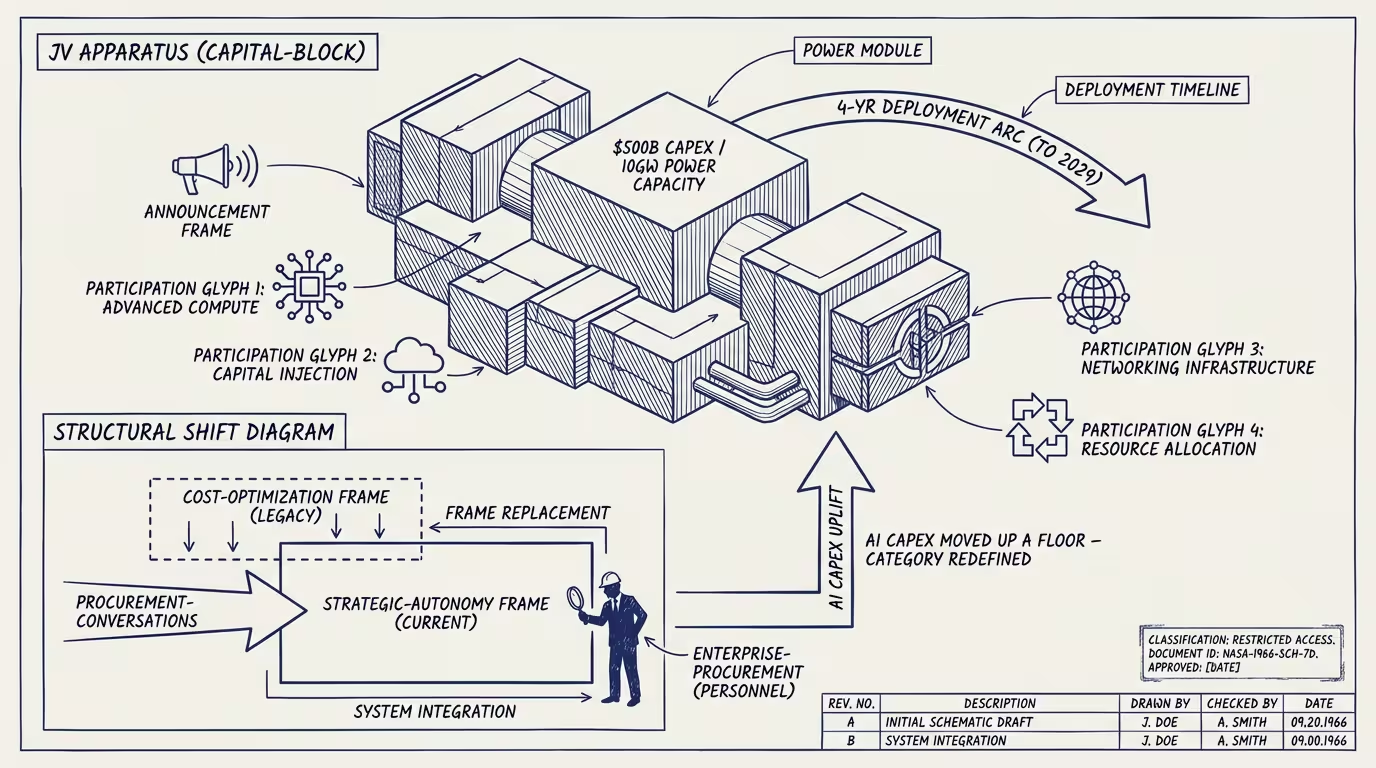

Stargate is industrial policy. AI capex moved up a floor.

The Stargate Project announcement at the White House on January 21, 2025: $500 billion over four years, 10 gigawatts of AI infrastructure deployed by 2029, joint venture between OpenAI, SoftBank, Oracle, and MGX. Trump introduced it. Altman, Son, and Ellison stood on stage. The press cycle wrote it up as the largest AI infrastructure announcement in U.S. history.

The number is real. The structural shift is what the announcement enabled, not what the announcement was.

The shift: AI capex moved up a floor.

Through 2024, AI infrastructure spend was a corporate-capex line item. Hyperscalers committed multi-billion-dollar build budgets in their earnings calls. The financial press tracked the spend at the company level. The Sequoia Cahn $600B essay framed the spend as a corporate-economics question. The Goldman Covello brief framed it as a corporate-economics question. The conversation was, in operating terms, between hyperscaler CFOs and their shareholders.

Stargate moved the same conversation up a floor.

The Stargate announcement is, in form, an industrial-policy announcement. The President is on stage. The framing is national-strategic. The funding is private but the imprimatur is federal. The 10 GW number is calibrated to AI-data-center demand projections, but the political framing is calibrated to Cold-War-era industrial-mobilization rhetoric.

Once the political framing lands, the operating shape of every adjacent decision changes.

Federal procurement.Federal customers (DOD, DOE, civilian agencies) procure AI infrastructure on a different framework if AI infrastructure is industrial policy than if it is corporate capex. The strategic-autonomy frame becomes the default procurement justification. The cost-optimization frame compresses. Federal contracts that would have been awarded on lowest-evaluated-bid criteria get awarded on national-strategic-fit criteria. Operators who pre-built the strategic-autonomy positioning capture more federal share.

Regulatory pacing.Regulatory frameworks treat industrial-policy categories differently from corporate-capex categories. Antitrust scrutiny softens (the regulator does not want to break up an industrial-policy build). Permitting pacing accelerates (the political class wants the build to ship). State-level utility commission approvals for AI-data-center transmission upgrades move faster. Permits for nuclear restart, for SMR deployment, for grid-interconnection priority all move on the industrial-policy calendar rather than the corporate-procurement calendar.

Capital availability.Sovereign-wealth-fund and pension-fund LP allocation toward AI infrastructure increases when the category is framed as industrial policy. The Saudi PIF, the Norwegian Government Pension Fund, the Canadian CPPIB all have explicit policy frameworks for industrial-policy-aligned investment that they do not have for corporate-capex investment. Stargate's $500B target is, in operating terms, an explicit invitation for sovereign LP allocation that the prior framing did not enable.

Geopolitical positioning.The Stargate announcement is a positioning move against Chinese AI infrastructure. The framing locks the U.S. into a strategic-competition posture that the corporate-capex frame did not. Adjacent decisions (export controls, chip-fabrication subsidies, foreign-investment review) get repriced against the national-strategic frame.

The part that holds is two-part.

Part one: any operator selling AI services to federal customers in 2025-2027 has to lead with the strategic-autonomy frame, not the cost-optimization frame. The procurement officer evaluating the operator's pitch is now operating under a framework where strategic-autonomy is the load-bearing criterion.

Part two: any operator competing with Stargate-aligned vendors has to recognize that the competition is now political-influence-shaped rather than purely market-shaped. OpenAI has the proximity. Anthropic, Google, Meta do not (yet). The Stargate-adjacent vendors are operating with a federal-procurement advantage the others have to work around.

The thing that crosses pillars is that industrial policy gets borrowed across categories. Healthcare-AI gets framed as strategic-autonomy in the next eighteen months. Travel/transportation infrastructure gets framed similarly. Energy-grid investment is already there. The pattern compounds.

The read that survives is that Stargate moved AI capex from corporate-capex to industrial policy on January 21, 2025, the framing has not yet been internalized by every operator in the category, and the operators who internalize it first are the operators who win the federal-customer procurement cycle in 2025-2027.

Stargate is industrial policy. AI capex moved up a floor. The procurement conversation moved with it. The operators who pre-built the strategic-autonomy positioning are the operators winning the federal contracts that the cost-optimization-positioned operators are about to lose.

—TJ