The Seam That Ate a Decade

In the "Suggestions for further research" section of my 2007 MA thesis, I buried a footnote about cross-jurisdictional health and insurance friction. The framing was academic, which is to say careful and muted. I noted that the movement of people across provincial and national boundaries created structural gaps in health coverage that existing systems weren't designed to handle, and that this was an under-studied area worth someone's attention.

I became that someone. It took about five years to understand what I'd actually pointed at, and another eight to operate inside it at scale.

This is the post-exit note I didn't write while I was building. Not the version I'd show investors (that version existed and served its purpose) but the version for people who want to understand what the seam actually looks like from the inside.

---

What the footnote got right

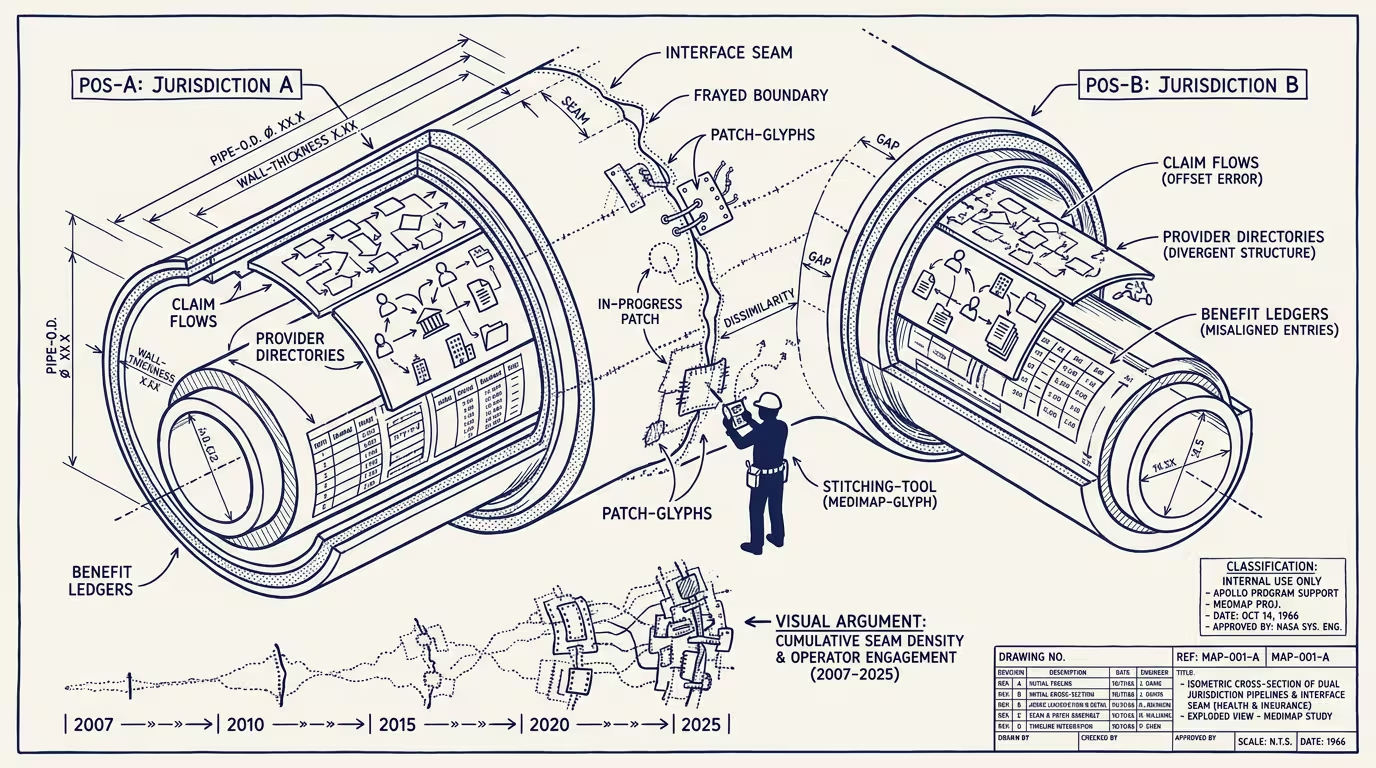

The cross-jurisdictional gap in health is not primarily a technology problem. It is not primarily a data problem. It is a structural problem that wears a technology costume and, occasionally, a regulatory one.

Here is what the structure actually looks like. Canada operates 13 distinct provincial and territorial health systems. Each province determines its own coverage, its own billing codes, its own definitions of what counts as insurable and what doesn't. A Canadian who moves from Ontario to British Columbia, or who spends six months in the United States, or who needs care in a province where they're not registered, falls into a gap that the systems were not built to bridge. Not because the systems are incompetent (many of the individual provincial systems are remarkably well-designed for what they were designed for) but because they were designed in an era when the assumption was that people stayed put.

People do not stay put these days. The 2007 thesis was largely about that fact.

What this creates, practically, is a landscape where the patient-navigation problem ("where do I get care, and what will it cost me, and who pays, and how long do I wait") is genuinely difficult to answer in a consistent way. The answer changes depending on which side of a provincial border you're on, what your insurance situation is, whether you're a registered patient of a family doctor in that jurisdiction, and whether the care you need falls under provincial coverage or private supplemental insurance.

Medimap was built in the middle of this. Canada's largest healthcare marketplace, at its peak serving tens of millions of users across the country, with a portfolio that covered walk-in clinic availability, appointment booking, and more, was at its core a navigation layer for people who couldn't easily answer that question themselves. The thing it did right was take a genuinely fragmented supply landscape (thousands of clinics, independent practitioners, pharmacies, specialist waitlists) and make it legible to someone who just needed to know where they could get care today.

What we learned, at scale, is that the bottleneck was almost never the care delivery side. It was the insurance and coverage question that sat upstream of it.

---

Why insurance is the actual problem

There is a version of the Canadian healthcare system narrative that says the problem is access, the problem is wait times, the problem is too few doctors. All of those things are real and potential topics for the future. But what I watched, operationally, at the marketplace level, was that a significant fraction of the friction for users had nothing to do with whether care was available. The care was often available, just somewhere that was either inconvenient or unknown. The friction was in the question of whether it was covered, and by whom, and what the out-of-pocket implication was for this particular person at this particular point in time.

The Canadian supplemental insurance market — the private layer that sits above provincial coverage and handles dental, vision, drugs, paramedical services, and care accessed out-of-province — is fragmented in ways that create genuine navigational complexity for users. An individual might have employer group benefits, a spouse's employer group benefits, provincial coverage, and a travel insurance policy, and have no reliable way to know, before an appointment, which of those applies to the thing they need and in what order. Or if and how they can be optimized per-claim, or policy-wide, based on their actual healthcare needs.

What this means for anyone trying to build a healthcare marketplace, or a navigation product, or an AI triage tool, is that the question "can you get care here" is actually three or four questions in sequence: is this service available, is the wait acceptable, is it covered, and at what cost to you specifically. The last two questions require insurance context that is usually not in the system you're operating in.

This is the seam the 2007 footnote pointed at. It is not a Canadian problem specifically (the US has a more acute version of the same dynamic, and the cross-border version compounds both systems' individual complexity) but Canada has a particular version of it that I understand in detail, and the Medimap experience gave me years of data about what happens when you try to build a product that sits in the middle of it.

---

Why direct-to-consumer healthcare keeps failing in Canada

There is a pattern in Canadian healthtech that I have watched repeat often enough to believe it's structural rather than coincidental. A well-funded company builds a direct-to-consumer healthcare product, achieves meaningful traction, runs into a reimbursement ceiling, and either pivots to the B2B (employer or insurer) channel or exits.

The consumer channel in Canada is not a great business for primary and preventive care, and the reason is that the provincial insurance framework creates a ceiling on what Canadians are accustomed to paying out of pocket for insured services. If something is provincially insured, the expectation is that cost is effectively zero at point of service. If it's not provincially insured, there's a well-established market for supplemental coverage, but that coverage is typically adjudicated through an employer plan, not a consumer app.

This creates a structural mismatch for D2C healthcare products that try to charge consumers directly for care or navigation services that sit adjacent to, but not inside, provincial coverage. The product may be genuinely useful. The willingness to pay is often low, not because the value isn't there, but because the frame of reference, care that costs nothing, is so deeply embedded in the consumer's mental model.

The organizations that have cracked Canadian healthcare at scale have almost all done so through B2B channels: employers, insurers, provincial health authorities. The consumer layer is a real market, but it is a smaller and more contested market than it appears from the outside, and it has a cultural resistance to direct payment for care that is not going to be resolved by product design.

The AI-mediated triage opportunity, which I think is real and coming faster than the industry expects, is likely to follow the same channel logic. It will be deployed first through B2B (employer wellness platforms, insurer intake systems, provincial virtual-care infrastructure) before it reaches the consumer as a standalone product. The companies building AI-first healthcare navigation tools for the D2C channel should think carefully about their distribution model before they think about their model architecture.

---

What AI actually changes, and what it doesn't

The PHIPA/HIPAA conversation, Canadian privacy law versus US privacy law, and the friction that creates for any company trying to operate across the border, tends to get framed as a regulatory problem. It is not primarily a regulatory problem. It is a data structure problem that the regulation makes legible.

The underlying issue is that Canadian and American healthcare data are not just governed differently; they are structured differently, coded differently, interoperable only partially and expensively, and anchored to different assumptions about what a "patient record" is and who owns it. A company that wants to do something useful with AI across the Canadian-American healthcare seam will spend a meaningful fraction of its engineering effort on this problem before it can do anything clinically interesting.

What AI changes (genuinely and meaningfully) is the navigation layer, not the coverage layer. An AI system can synthesize the complexity of provincial coverage rules, supplemental insurance structures, and availability data in a way that was previously too expensive to do at the individual user level. That is a real capability improvement. It's what I would have done with it in 2022 if the tools had been there.

What AI does not change is the underlying fact that a claim still has to be adjudicated against a real insurance policy, that a billing code still has to match the jurisdiction's coverage schedule, and that the legal and financial infrastructure for cross-border care is still built on frameworks that were designed for humans moving slowly, not agents moving fast.

The companies that will do interesting things with AI in Canadian healthcare over the next five years will be the ones that treat the coverage complexity as a product challenge, something to be encoded, navigated, and surfaced, rather than a regulatory obstacle to wait out. The regulatory environment in Canada is not going to change fast enough to be the unlock. The data architecture and the AI capability meeting in the middle of the insurance layer: that's where the opening is.

---

What I'd tell the 2007 footnote

What follows is addressed to the 2007 version of me, and to the footnote I left in his MA thesis. I am using the second person on purpose. The piece up to this point has been operator voice; this final section steps out of it deliberately, because the footnote was a question, and a question deserves an answer in the voice it was asked.

The gap you flagged was real. You built inside it for a decade, and the experience confirmed several things: that the gap is structural and persistent, that it is primarily an insurance problem rather than a care-delivery problem (or at least a 60/40 split), that the consumer channel is vastly harder than it looks and the B2B channel is more durable than it appears from the outside, and that the AI-mediated navigation layer is genuinely possible now in ways it wasn't during the Medimap years.

It also confirmed the thing the footnote implied but didn't say directly: that the people who move across these jurisdictional seams are not edge cases. They are the bellwether. What fails for them, eventually fails for everyone, because the gap is not a gap at the border, it is a gap in the assumption that the patient and the system will always be in the same place at the same time.

That assumption is wrong. I knew it in 2007. I know the shape of how wrong it is now, in a way that requires considerably more words than a footnote.

—TJ