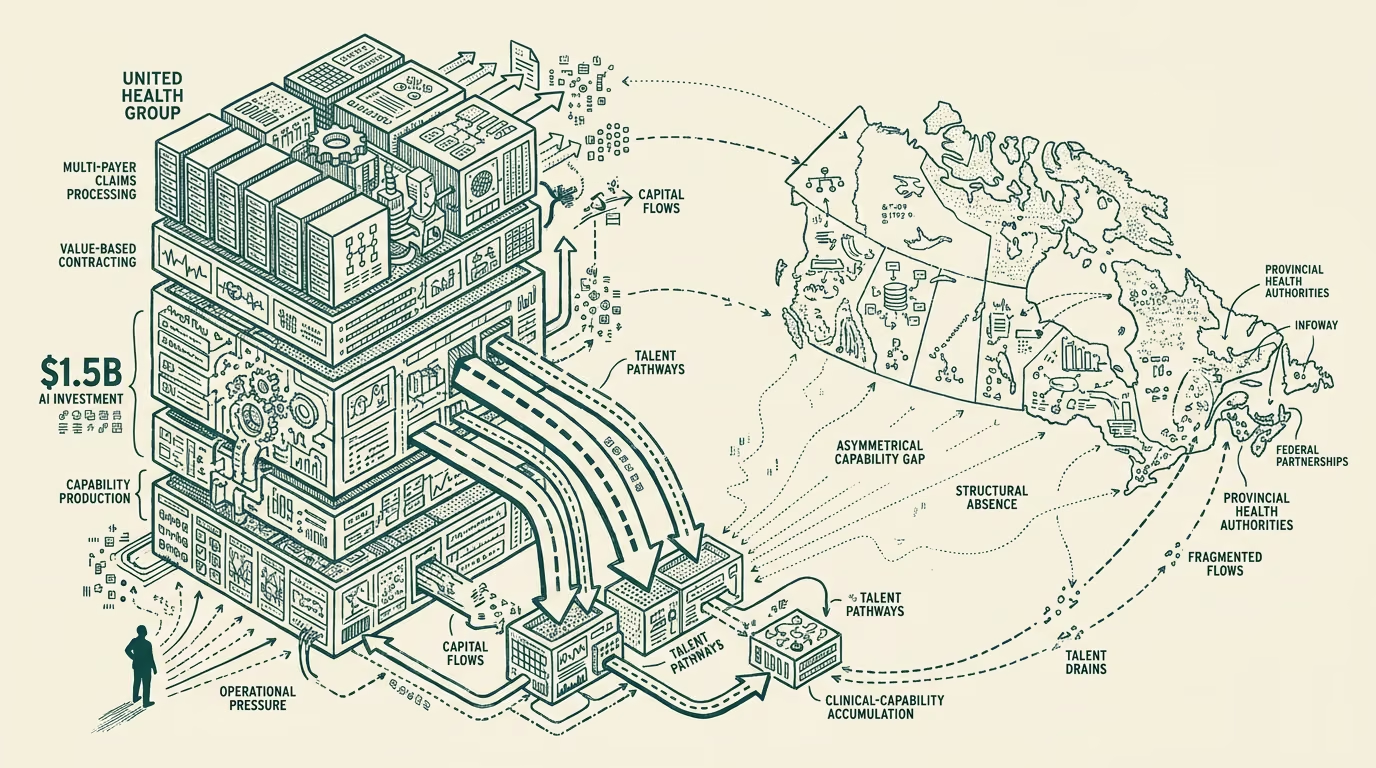

UnitedHealth invested $1.5B in AI. No Canadian payer invested anything equivalent. That gap compounds.

UnitedHealth Group's April 2026 announcement of approximately $1.5 billion in AI capex through 2026-2027 sits as a public commitment in the U.S. payer landscape with no equivalent on the Canadian side. The largest Canadian provincial health authority's AI investment, summed across the publicly-disclosed lines, runs in the tens of millions of dollars per year. Canada's federal-level AI investment in healthcare, channeled through Canada Health Infoway and the various provincial-federal partnerships, runs at a similar scale. The combined Canadian healthcare-AI investment line, summed across the public-and-payer side, runs at perhaps 5-10 percent of UHG's single-vendor commitment.

The Canadian framing on the gap sometimes reads it as appropriate. The single-payer system does not face the same operational pressures that drive U.S. payer AI deployment. The administrative-cost line that absorbs much of the U.S. AI investment is structurally smaller in Canada because the multi-payer-claims-processing infrastructure that U.S. payers run does not exist. The clinical-quality-measurement framework that U.S. payers use to drive value-based-care contracts is similarly less central in Canada. The framing concludes that the gap is structurally appropriate.

The structural read is that the gap is real and compounds for international capital allocation, talent acquisition, and longer-cycle clinical-AI capability building, and that the appropriate-gap framing under-prices the cost of the investment shortfall. This essay walks both readings, names where each is right and wrong, and lays out what the durable read on the gap should be.

What UHG actually invested in

The UHG $1.5B AI capex commitment, based on the public communications, covers four specific investment lines. The first line is the claim-routing-and-adjudication infrastructure, which automates substantial portions of the multi-payer claims processing the company runs at scale. The second line is the clinical-decision-support tooling deployed across the company's provider-side businesses (Optum), with substantial integration into the EHR-and-clinical-workflow infrastructure. The third line is the prior-authorization-and-utilization-management automation, which addresses the operational friction that has been a sustained regulatory-and-public-relations issue for the company. The fourth line is the broader AI-augmented operations infrastructure across the rest of the company's operating footprint, including the population-health-management work, the post-discharge-engagement programs, and the various care-coordination workflows.

Each line is operationally tied to a specific cost-and-revenue trajectory the company expects to capture. The investment is not speculative; it is sized against documented operational ROI in each category.

Where the appropriate-gap framing is right

The appropriate-gap framing has several genuine strengths.

The U.S. multi-payer claims-processing infrastructure is structurally larger than the Canadian equivalent because the U.S. has hundreds of payers and the Canadian system has provincial single-payers. The investment in claims-routing-and-adjudication AI in the U.S. is responding to an operational complexity that does not exist in Canada at the same scale.

The U.S. prior-authorization workload is structurally larger than the Canadian equivalent because the U.S. private-insurance model produces utilization-management work that the Canadian public-system does not produce in the same shape. The investment in prior-auth automation is, again, responding to U.S.-specific operational complexity.

The U.S. value-based-care infrastructure that drives clinical-quality-measurement-and-AI investment is structurally larger than the Canadian equivalent because the U.S. has a substantial value-based-care contracting economy that the Canadian system does not run.

The combined effect is that the U.S. payer-class faces operational complexity in several specific dimensions that the Canadian payer-class does not face, and the AI investment in those dimensions is appropriately concentrated on the U.S. side. The straight-comparison that produces the gap headline is, in this sense, comparing AI investment against differently-shaped operational footprints.

Where the structural-cost framing is right

The structural-cost framing has its own strengths, and the appropriate-gap framing under-prices several lines of cost the gap produces for Canada.

The first line is the talent-and-capability-building cost. U.S. payer-class AI investment at UHG scale produces substantial career opportunities for Canadian healthcare-AI engineers and product leaders. The talent migrates to where the investment is. Canadian healthcare-AI talent at the senior level has been migrating south for several years, and the UHG-class investment lines accelerate the migration. The talent migration produces a longer-cycle capability gap that compounds because the Canadian healthcare-AI ecosystem has progressively fewer senior people to anchor the next generation.

The second line is the international-capital-allocation cost. Investors and strategic partners evaluating Canadian healthcare-AI companies and Canadian healthcare-AI ecosystem investment compare the Canadian environment to the U.S. environment, with the U.S. environment increasingly anchored by visible payer-class capex commitments at the UHG scale. The Canadian environment, with the public-tier investment running an order of magnitude smaller, looks structurally less serious to the international capital. The capital allocation that follows reflects the perception, with Canadian healthcare-AI companies receiving lower valuations, slower deployment of partnership capital, and tighter terms. The gap compounds because the capital trajectory shapes the next-cycle ecosystem.

The third line is the longer-cycle clinical-AI capability building. The clinical-AI work that produces durable competitive advantage for a healthcare system is multi-year work that requires sustained investment in the data infrastructure, the eval-and-validation framework, the clinician-and-team training, the regulatory-and-compliance posture. UHG's $1.5B commitment is sized to support this multi-year work. The Canadian payer-class does not have an equivalent commitment, with the consequence that the longer-cycle clinical-AI capability building is structurally underfunded and the resulting capability gap compounds across the foreseeable horizon.

The combined effect is that the appropriate-gap framing, while right that the operational-complexity dimension is different, under-prices the talent-migration, capital-allocation, and longer-cycle-capability-building costs that the Canadian system absorbs from the gap.

What the operator class should take from this

For Canadian healthcare-AI operators, the part that holds is that the public-tier investment trajectory is unlikely to close the gap meaningfully on the relevant timeline, and the strategic posture should be calibrated against the durable gap rather than against the imminent-investment scenario. Operators should plan against the international-capital-allocation pattern that the gap produces, with the implication that Canadian healthcare-AI companies will need to compensate through stronger product-and-market positioning, deeper international-customer-acquisition, and tighter operating-leverage discipline than U.S. peers.

For Canadian provincial health authorities and federal agencies evaluating the AI-investment question, the operator-class read is that the appropriate-gap framing under-prices the longer-cycle costs and that the public-investment trajectory should be revisited with the compounding-cost dimension priced in. The current trajectory leaves Canada structurally behind on capability, talent, and capital trajectory, with the compounding effects making the position progressively harder to recover from each year the gap continues.

For international investors evaluating the Canadian healthcare-AI ecosystem, the structural read is to price the gap accurately rather than against the appropriate-gap headline. Canadian healthcare-AI investments face structural headwinds that U.S. equivalent investments do not face, and the valuation framework should reflect this. The headwinds are real and durable.

What might close the gap

A small set of moves could meaningfully close the gap if pursued with discipline. The first is meaningful federal-and-provincial public investment in the AI-infrastructure-and-data-platform layer that supports the longer-cycle capability building. The investment scale required is in the multi-billion-dollar range over a multi-year window, with the work concentrated on the data-portability infrastructure under Bill C-72 plus the AI-evaluation-and-deployment infrastructure that operates against the data layer. The investment is politically difficult but operationally tractable.

The second is structured talent-retention work. Programs that compete with the U.S. payer-class on senior healthcare-AI talent require visible federal-and-provincial commitment, not just pricing. The retention work involves career-trajectory planning, research-and-deployment opportunities, and the broader ecosystem-building that anchors talent in place. The investment is multi-year and meaningful.

The third is international-partnership work that imports the capability the Canadian system is structurally underfunded to build internally. Partnerships with U.S. payer-class entities, with the major foundation-model vendors, with the international-tier healthcare-AI players, can substitute for some of the gap if structured carefully. The partnership work has its own risks (data-sovereignty, regulatory-class concerns, the longer-cycle capability-dependence the partnerships create) that need to be priced.

The combined moves can substantially close the gap if pursued with sustained commitment across multiple political cycles. The appropriate-gap framing tends to argue against the moves because it under-prices the structural costs. The structural read on the longer-cycle compounding suggests the moves are necessary, with the recognition that they are politically and operationally difficult.

The UHG $1.5 billion commitment is the visible benchmark that the Canadian system does not have an equivalent of. The gap is real, the appropriate-gap framing is partial, the structural-cost framing is closer to the full picture, and the structural read on the next 24-36 months should price the gap as a durable feature of the Canadian healthcare-AI environment that operators need to plan around. The gap compounds. The cost is real. The work to close it is the work the political-and-investment class should be undertaking now, while the trajectory is recoverable.

—TJ